Stop Paying Interest on a Life You Can't Afford — Get a Clear 14-Day Plan to Escape the Minimum Payment Trap and Finally Breathe Again

BreatheBudget is a step-by-step 14-day cashflow triage guide for Americans with $2K–$10K in credit card debt who are done watching their paycheck vanish into minimum payments — with ready-made scripts, simple decision trees, and zero extreme budgeting required.

See real breathing room in 14 days — without waiting years to become debt-free or overhauling your entire lifestyle

Stop bleeding money on fees, APR, and bill creep you didn't even know were draining you every single month

Negotiate your interest rates and bills with confidence — using word-for-word phone scripts so you never freeze up or get stonewalled

Build a payoff path that actually sticks — snowball or avalanche, automated and guardrail-protected, no spreadsheet PhD required

No shame, no lectures, no "just stop buying coffee" — only practical micro-actions you can take this week, even when life gets messy

Works around your real paycheck schedule — bi-weekly, semi-monthly, or irregular income, the plan adapts to you

Identify your "invisible leaks" in 30 minutes — the subscriptions, banking fees, and lifestyle creep quietly costing you hundreds a year

🎉 $134.00 ➝ JUST $27.00 (80% OFF — Save $107.00)

✅ Instant Access + 5 FREE Bonuses

🔐 One-time payment – No subscriptions!

Secure Payments - 14-Day Guarantee - Instant Download

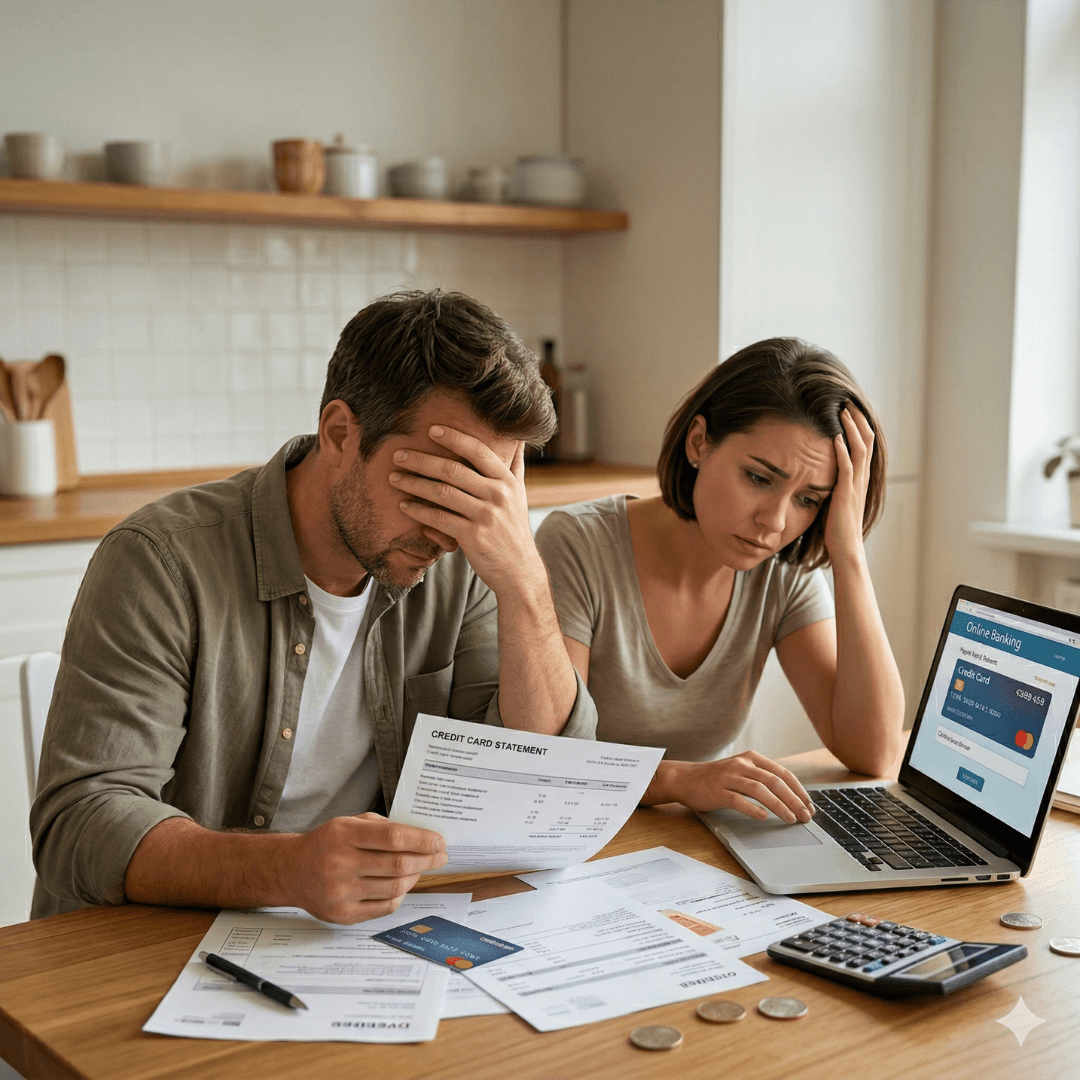

The Minimum Payment Trap Is Not Your Fault — But It Is Costing You Every Single Month

You open the credit card statement.

You see the balance.

You feel that familiar drop in your stomach.

You pay the minimum — because that's what you can do — and you tell yourself things will be different next month.

But next month comes, and the balance barely moved. The interest ate most of what you paid. Another $35 late fee appeared out of nowhere. And now you have $200 less to work with before the next paycheck even hits.

This is the minimum payment trap — and it is designed to keep you in it.

Here's what's really happening beneath the surface:

Most credit card companies charge 22%–29% APR. When you carry a $4,000 balance and pay the minimum, you're sending them $80–$100 a month… and maybe $15 of that actually reduces your debt. The rest is pure profit for them.

Meanwhile, you're dealing with:

Bill creep — your streaming subscriptions, phone plan, and insurance all crept up 10–15% this year, and you barely noticed

Fee drip — overdraft fees, annual card fees, paper statement fees eating $30–$60 a month you'll never get back

Decision fatigue — by the time Friday hits, you're too exhausted to track anything, so you swipe and deal with it later

And the worst part?

The advice you keep getting makes it worse.

"Make a budget." — You've tried. Life doesn't run on a spreadsheet.

"Cut your lattes." — You already cut the lattes. It didn't move the needle.

"Pay off the highest-interest card first." — Great idea, but which card? With what money? And what happens when the car breaks down in month two?

The problem isn't discipline. It's not willpower. It's not that you're "bad with money."

The problem is you've never had a triage plan — a system to stop the bleeding first, before anything else.

Because when you're losing $200–$400 a month to invisible leaks, high APR, and minimum payment math, no budget in the world will save you. You need to plug the holes before you start bailing water.

That's exactly what BreatheBudget was built to do.

Introducing BreatheBudget: The 14-Day Cashflow Triage Guide That Stops the Bleeding and Gets You Breathing Again

BreatheBudget is not a budgeting book.

It's not a "get out of debt in 12 months" fantasy program.

It's a 14-day operational triage — a day-by-day action guide that takes you from "paycheck panic" to a clear, sustainable payoff path using only micro-actions, ready-made scripts, and simple decision frameworks.

Here's what the 14 days actually look like:

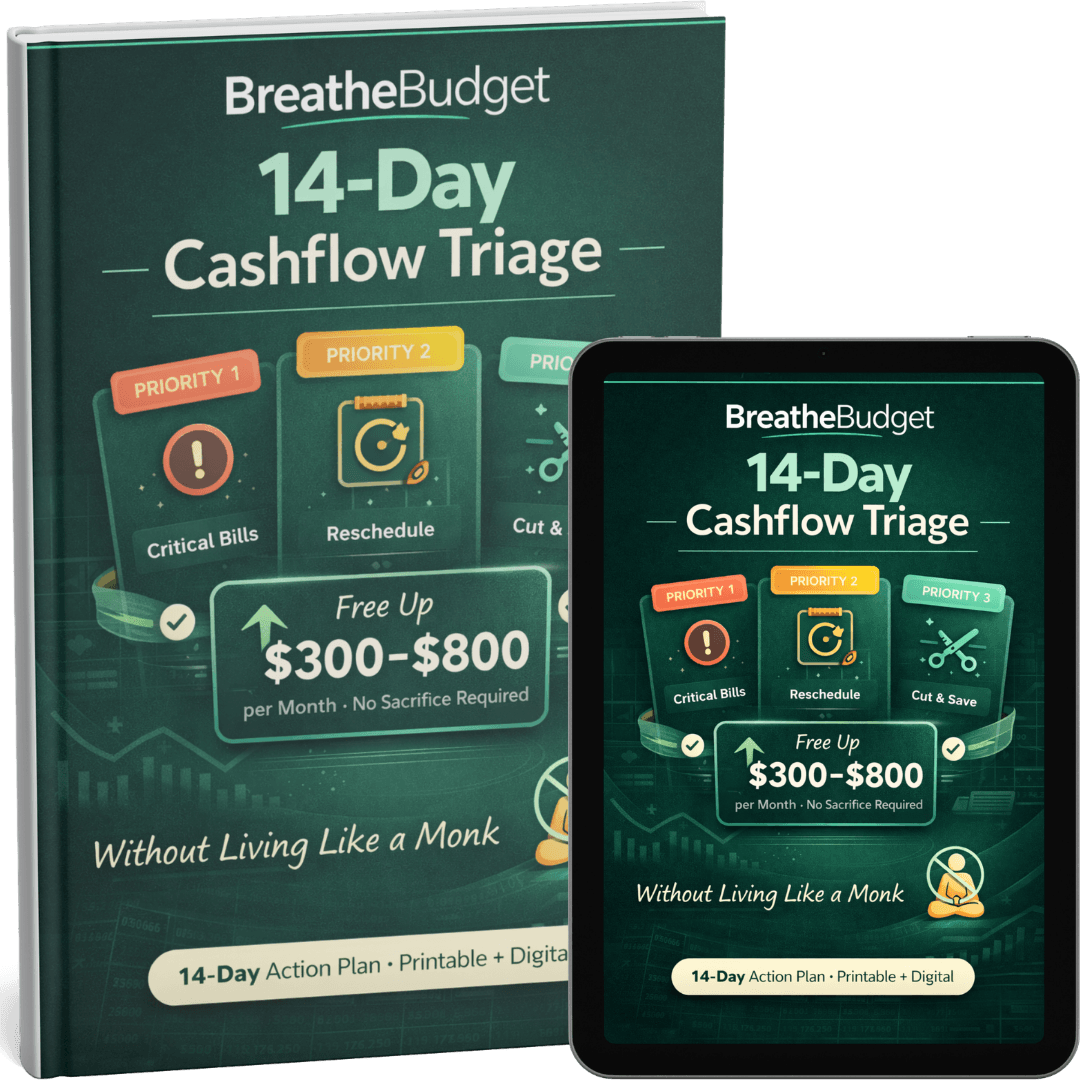

Days 1–3: Cash Flow Triage

You map every dollar going out. Not to judge yourself — to find the leaks. Subscriptions you forgot about. Fees that have been auto-charging for 18 months. Bill increases that snuck in. You use the included audit framework to pinpoint exactly where your money is disappearing.

Days 4–7: Stop the Bleeding

You take your first real actions. You cancel what doesn't serve you. You call your credit card company and ask for an APR reduction — using the exact script included in the guide. You call your internet or phone provider and negotiate a lower rate — again, with the script. These calls take 10–15 minutes and can free up $50–$150 a month starting immediately.

Days 8–11: Build the Payoff Path

Now that you've stopped the bleeding, you have actual breathing room. You choose your payoff method — snowball (smallest balance first for quick wins) or avalanche (highest APR first to save the most money) — and you set up the minimum automations to keep it moving without you having to manually manage it every week.

Days 12–14: Install the Guardrails

Life will happen. The car will need a repair. A surprise bill will arrive. BreatheBudget gives you the decision tree for those moments so you don't blow the whole plan when reality hits. The guardrails are simple rules that keep you on track without requiring perfection.

What you get inside BreatheBudget:

✔ The full 14-day day-by-day action guide (PDF + digital, printable)

✔ The 30-Minute Cash Flow Audit framework to find your leaks fast

✔ Word-for-word phone scripts for APR negotiation, bill reduction, and fee waiver calls

✔ The Minimum Payment Escape Calculator — see exactly what your payoff date looks like under each strategy

✔ The Payoff Path Builder — snowball vs. avalanche comparison with your real numbers

✔ The "Life Happens" Decision Tree — what to do when an unexpected expense threatens to derail you

✔ The BreatheBudget Daily Check-In (5 minutes/day) — so you stay consistent without obsessing

✔ 5 FREE Bonuses (see below)

This is the operational guide you needed three years ago — but it works just as well starting today.

Why the Minimum Payment Escape System™ Works When Every Other Method Has Failed You

Here's the painful truth no personal finance guru wants to admit:

Most debt advice is built for people who are already stable.

"Max out your Roth IRA." — Cool. What about the $47 overdraft fee this week?

"Follow the Dave Ramsey Baby Steps." — Great framework. Except Baby Step 1 assumes you have cash to spare. You're in triage.

"Use the avalanche method." — Mathematically optimal. Emotionally brutal when you see zero visible progress for 6 months.

The advice isn't wrong. It's just built for someone else's financial situation — not yours, not right now.

The Minimum Payment Escape System™ is different because it sequences the work correctly.

Here's the core logic:

Most people try to fix their spending habits before they've fixed their cost structure. But if you're paying 26% APR on a $3,500 balance and have two subscriptions charging you for services you don't use — no habit change in the world will overcome that math.

The Minimum Payment Escape System™ follows a specific three-phase sequence:

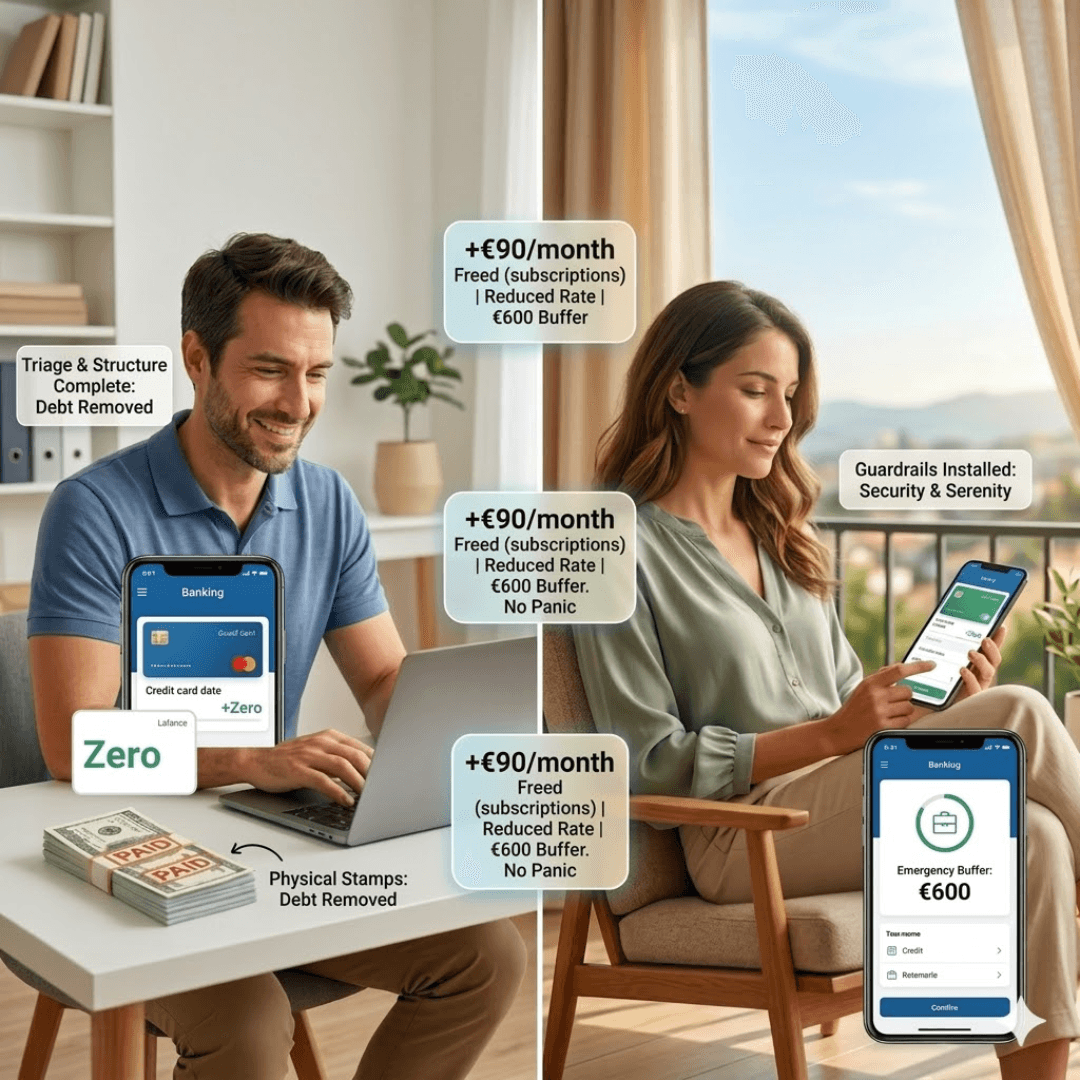

Phase 1 — Triage (Days 1–7): Find and eliminate the invisible losses. Not by cutting your lifestyle to the bone — but by surgically removing the waste and negotiating the costs you're overpaying. This phase alone typically frees up $75–$200/month for people who apply it fully.

Phase 2 — Structure (Days 8–11): Build the payoff path on top of the breathing room you've just created. This is the only moment in the sequence where budgeting advice actually lands — because now there's slack to work with.

Phase 3 — Guardrails (Days 12–14): Install the behavioral fail-safes that keep the system running when life gets unpredictable. The 24-Hour Rule. The Weekly Check-In. The Spending Cap by category. The Card Freeze protocol. These aren't restrictions — they're decision shortcuts that remove the need for willpower.

Why this works when willpower doesn't:

The Minimum Payment Escape System™ is not asking you to become a different person. It's not asking you to have more discipline, more time, or more financial knowledge.

It's asking you to follow a sequence — the right actions, in the right order, at the right time — with the exact scripts and tools you need to execute each step.

When the sequence is correct, the results compound. A $90/month freed from cancelled subscriptions + a $40 APR reduction + a $600 emergency buffer = you are no longer one bad week away from financial panic.

That's what breathing room actually feels like.

🎁 Your Complete BreatheBudget Bundle Includes:

📘 MAIN GUIDE — BreatheBudget: 14-Day Cashflow Triage to Escape the Minimum Payment Trap

VALUE $47.00 INCLUDED!

The guide covers 14 days of work — but it's structured as a triage, not a transformation. Day 1 isn't "set your goals." Day 1 is "find the money that's already leaving your account for no good reason." From there, every step builds on the last until you have a payoff path running on its own.

✔ Know exactly where your money is going — and stop the leaks that have been draining you for months without you noticing

✔ Free up real cash every month starting in the first week — before you touch your spending habits or cut anything you actually care about

✔ Get your APR and bills reduced using scripts that do the talking for you — no negotiation experience required

✔ Build a payoff path that fits your real income schedule — not a theoretical monthly budget that falls apart by Day 3

✔ Stay on track when life gets in the way — with a decision framework for unexpected expenses that keeps the plan intact

✔ See your progress in black and white — so "am I actually getting anywhere?" stops being a question you dread

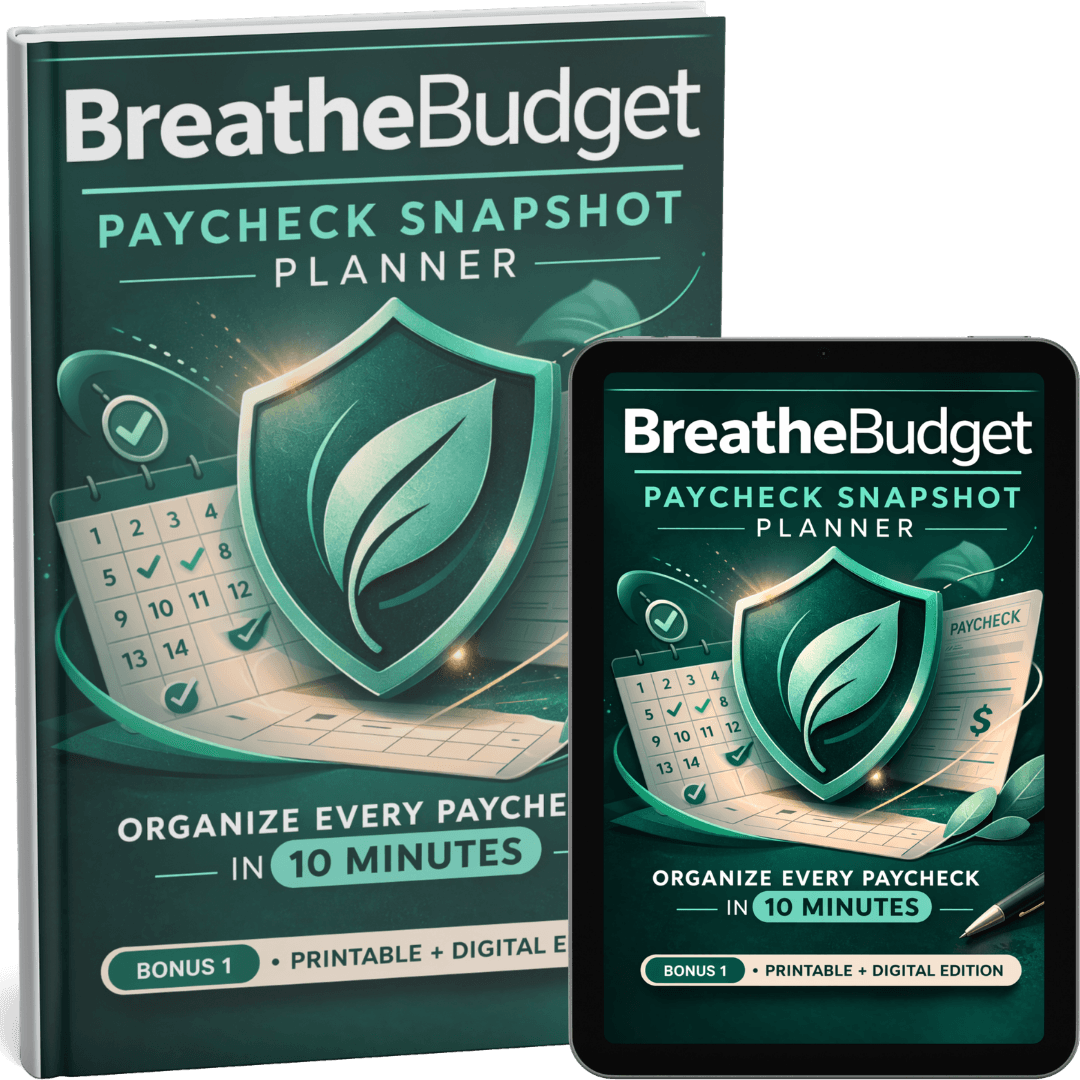

🎁 BONUS 1 — BreatheBudget Paycheck Snapshot Planner

VALUE $19.00 INCLUDED!

A fillable planner (PDF + digital version) that maps every paycheck — bi-weekly, semi-monthly, or irregular — to your real expenses in under 10 minutes. So nothing gets missed while you're running the 14-day triage.

✔ Built for real-world income schedules, not idealized monthly budgets

✔ Aligns rent, bills, and card payments to your actual cash arrival dates

✔ Color-coded priority columns so you always know what hits first

✔ Reusable — one template per paycheck, reset every cycle

✔ Pairs directly with Days 8–11 of the BreatheBudget plan

🎁 BONUS 2 — Invisible Leaks Playbook (Mini-Ebook)

VALUE $17.00 INCLUDED!

A focused 20–30 page mini-ebook that maps the three categories of financial leaks draining your account every month — subscriptions & apps, lifestyle leaks, and banking & fee creep — with real-world examples and a printable checklist to track exactly what you find, cut, reduce, and save.

✔ Organized into 3 clear leak categories with concrete examples in each

✔ Includes the "Leak Audit Checklist" — mark what you found, what you cut, what you reduced

✔ Monthly savings column so you can see the real dollar impact of every decision

✔ Designed to be repeated every 90 days as a "financial tune-up"

✔ Works as a standalone deep-dive alongside Days 1–3 of the main guide

🎁 BONUS 3 — Debt Oxygen Tracker Planner

VALUE $22.00 INCLUDED!

A printable and fillable monthly tracker that lets you monitor your financial breathing room in real time — tracking balance, minimum payment, interest paid, cashflow freed, and monthly goal for every card and bill, with a visual color scale (red / yellow / green) to show your "oxygen level" at a glance.

✔ One tracker page per card/bill — keep them all in one place

✔ Visual oxygen scale makes progress impossible to ignore (or fake)

✔ Monthly goal field keeps you focused on one improvement at a time

✔ Shows you exactly where to apply extra pressure each month

✔ Turns the abstract feeling of "am I making progress?" into hard, visible data

🎁 BONUS 4 — 14-Day Action Prompts Pack

VALUE $12.00 INCLUDED!

A ready-to-use pack of daily prompts formatted for to-do apps, Google Calendar, and sticky notes — one per day of the BreatheBudget plan, in three tone variants (Soft, Direct, No-BS) so you can pick the style that actually gets you moving.

✔ 14 pre-written daily prompts — just copy and paste into your preferred system

✔ Three tone variants per prompt: choose what fits your personality and energy

✔ Eliminates decision fatigue — you never have to remember "what do I do today?"

✔ Designed to appear at the right moment, not require you to reopen the guide

✔ Turns the 14-day plan into a self-running reminder system

🎁 BONUS 5 — 30-Day Relapse-Proof Challenge

VALUE $17.00 INCLUDED!

A PDF mini-guide that extends the BreatheBudget work beyond the 14 days: 4 weeks of micro-challenges built around the core guardrails — the 24-Hour Rule, the Weekly Check-In, Spending Caps, and the Card Freeze protocol — with daily self-assessment sheets to catch backsliding before it becomes a setback.

✔ 4 weeks of structured micro-challenges to lock in new financial habits

✔ Daily self-assessment prompts (takes 2 minutes) — rate your own compliance honestly

✔ Weekly reflection spread to identify what's working and what needs adjustment

✔ Based on the same guardrail system built into the main BreatheBudget guide

✔ Prevents the #1 failure mode: stopping on Day 15 and losing all the progress

About the Creator: Marcus Calloway

Marcus Calloway spent most of his early thirties doing exactly what he tells people to stop doing: paying the minimum, telling himself he'd fix it "next month," and watching $200–$300 disappear every month into interest and fees he barely tracked.

He wasn't irresponsible. He was overwhelmed. Working a full-time job, dealing with an irregular side income, and trying to keep up with bills that seemed to grow on their own — he didn't need a lecture about discipline.

He needed a plan that actually matched his reality.

After years of testing different debt payoff strategies, negotiating his own APR cuts and bill reductions, and mapping what actually moved the needle versus what just created guilt — Marcus built the framework that became the Minimum Payment Escape System™.

BreatheBudget is the guide he wishes had existed when he was staring at a $6,400 credit card balance wondering where to even start.

Today, Marcus creates practical financial clarity tools for everyday Americans who are tired of advice built for people already on solid ground. His work focuses on one principle: stop the bleeding first, then build from there.

🔐 14-Day "Breathe First" Guarantee

Try BreatheBudget for a full 14 days — run the triage, use the scripts, complete the audit, and apply the plan to your real paycheck situation.

If at the end of those 14 days you haven't experienced at least one of the following:

✔ Identified at least one "invisible leak" costing you money you didn't know was leaving

✔ Successfully used a script to negotiate a bill, fee waiver, or APR reduction

✔ Installed a payoff path that actually fits your real income schedule

✔ Felt noticeably less panicked when you open your credit card app

…just send us an email within 14 days and you'll receive a full 100% refund.

No forms. No explanations required. No guilt.

You either get results, or you get your money back. That's the deal.

📦 Everything You Get Today for Just $27.00:

$ 134.00

$ 27.00

80% DISCOUNT + 5 FREE BONUSES

📘 Main Guide: BreatheBudget 14-Day Cashflow Triage — the full day-by-day operational plan with scripts, calculators, and decision trees

($47 value)🎁 Bonus 1: Paycheck Snapshot Planner — map every paycheck to real expenses in 10 minutes

($19 value)🎁 Bonus 2: Invisible Leaks Playbook — 20–30 page mini-ebook + printable audit checklist

($17 value)🎁 Bonus 3: Debt Oxygen Tracker Planner — monthly visual progress tracker per card/bill

($22 value)🎁 Bonus 4: 14-Day Action Prompts Pack — daily prompts in 3 tone variants, ready for any app

($12 value)🎁 Bonus 5: 30-Day Relapse-Proof Challenge — 4-week micro-challenge guide to lock in the habits

($17 value)

🎉 $134.00 ➝ JUST $27.00 (80% OFF — Save $107.00)

✅ Instant Access + 5 FREE Bonuses

🔐 One-time payment – No subscriptions!

Secure Payments - 14-Day Guarantee - Instant Download

F.A.Q.

Most debt tools are built around the assumption that you already have a stable, predictable cash flow — they just need you to "allocate" it better. BreatheBudget starts from a different premise: you may be hemorrhaging money through fees, invisible leaks, and high APR before you even get to "allocating" anything. The 14-Day Cashflow Triage is specifically sequenced to plug those holes first — and the included scripts give you immediate, actionable leverage (like APR reduction calls) that no app can do for you. It's not a tracker. It's an operation.

Absolutely — in fact, the lower your balance, the faster the Minimum Payment Escape System™ works. A $2,500 balance at 24% APR is still costing you $50+ a month in interest alone. One successful APR negotiation call (using the included script) can cut that in half immediately. The 14-day plan is calibrated to work at every level of the $2K–$10K range.

The BreatheBudget plan was built specifically for real-world income schedules — including bi-weekly, semi-monthly, and irregular income. The Paycheck Snapshot Planner (Bonus 1) helps you map each incoming paycheck to its specific obligations, so the plan adapts to your actual money arrival dates, not a theoretical monthly average.

The APR negotiation call is one of the highest-leverage actions in the entire plan — but it's also one of the most dreaded. That's why BreatheBudget includes a word-for-word phone script you can read directly from the page. You don't need to freestyle it or "know what to say." You read the script, answer their questions with the prepared responses also included, and either get the reduction or politely close the call. Most calls take 8–12 minutes. Even a partial APR reduction can free up $30–$80 a month.

BreatheBudget is focused primarily on credit card debt and monthly cashflow — but the "Stop the Bleeding" section covers negotiating phone bills, internet bills, insurance premiums, and banking fees as well. The Invisible Leaks Playbook (Bonus 2) specifically maps subscription and lifestyle leaks across all categories. If the expense shows up on your bank statement or credit card, BreatheBudget has a protocol for it.

The daily actions are designed around the reality that you have a job, possibly a family, and limited bandwidth. On heavier days (Days 1–3 for the audit, Days 4–7 for the negotiation calls), you'll need 30–60 minutes. On lighter days, the BreatheBudget Daily Check-In is 5 minutes. The 14-Day Action Prompts Pack (Bonus 4) is specifically designed to reduce your cognitive load — you don't need to re-read the guide each morning to know what to do.

Some calls won't succeed on the first attempt. The guide addresses this directly — including what to say when you get a "no," when to escalate to a supervisor, when to call back (timing matters), and when to simply accept the outcome and move to the next lever. Even if 2 out of 5 negotiation attempts succeed, you're still ahead. The plan isn't built on perfection — it's built on stacking small wins.

Yes. The Payoff Path Builder inside BreatheBudget walks you through both the snowball and avalanche methods across multiple cards — with your real balances and APR rates — so you can see exactly which card to target first and in what sequence. The Debt Oxygen Tracker Planner (Bonus 3) gives you a dedicated tracking page for each card so nothing gets lost or overlooked.

No extreme budgeting. No spending freezes across entire categories. No "rice and beans until debt-free" philosophy. BreatheBudget is built on a concept called guardrails — lightweight rules that create structure without demanding perfection. The 24-Hour Rule (wait one day before any non-essential purchase over a set threshold). The Weekly Check-In (10 minutes, Sunday). Spending Caps by category (you set them based on your real life). These aren't punishments. They're decision shortcuts that remove the need for constant willpower.

You have 14 full days from purchase to try everything — the triage, the scripts, the bonus planners, all of it. If you apply the plan and don't feel a genuine, noticeable improvement in your financial breathing room, just email us and you'll receive a 100% refund with no questions asked and no hoops to jump through. The guarantee is real. We're confident in the system — but if it's not right for you, you don't pay.